DeFi Llama data reveals that dozens of well-funded Layer 1 and Layer 2 blockchains are generating virtually zero fees and haemorrhaging users. We examine five of the biggest flops, explain why a handful of chains are thriving, and ask what separates the living from the dead.

Between 2023 and 2025, the cryptocurrency industry experienced a chain-building frenzy unlike anything in its history. Venture capital firms poured billions into new Layer 1 and Layer 2 blockchains, each promising to be faster, cheaper, or more innovative than the last. Founders raised nine-figure rounds on little more than a whitepaper and a pitch deck. Every protocol wanted its own chain. Every VC wanted exposure to the next Solana or Ethereum killer.

The logic was seductive. If Ethereum was congested and expensive, the market needed alternatives. If Solana could achieve breakout success, then surely there was room for ten more high-performance chains. And if you could attract developers with grants, users with airdrops, and liquidity with incentive programmes, the network effects would eventually become self-sustaining. Or so the theory went.

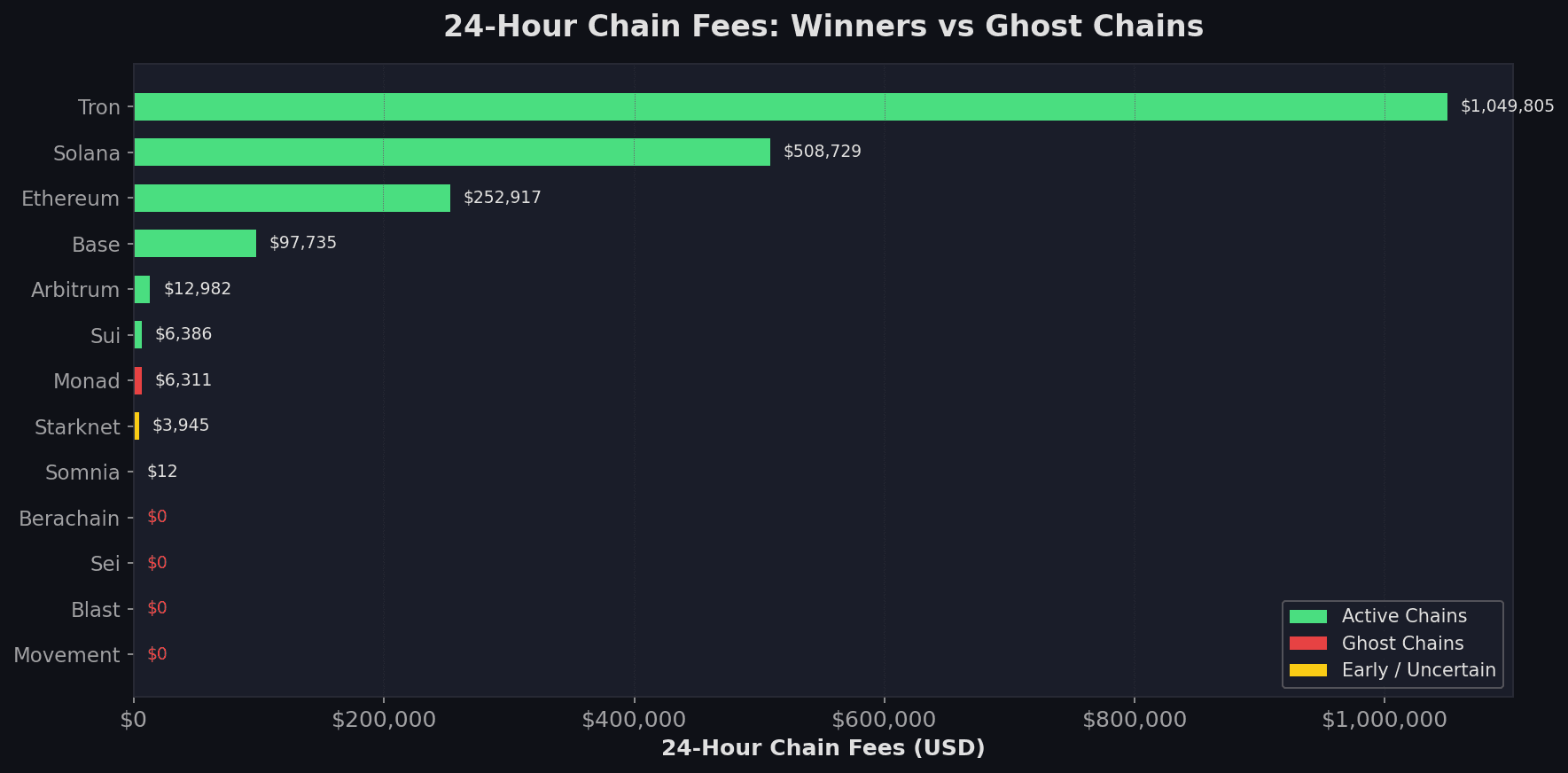

In April 2026, the data tells a very different story. Pull up DeFi Llama's chain rankings page and sort by 24-hour fees (the most honest measure of whether anyone is actually using a blockchain) and the picture is stark. A handful of chains dominate. Everything else is a rounding error.

The Numbers Do Not Lie

According to DeFi Llama data as of 7 April 2026, the top five chains by 24-hour fees account for the overwhelming majority of all blockchain economic activity. Tron leads with $1.05 million in daily fees, followed by Solana at $508,729, Ethereum at $252,917, Bitcoin at $148,833, and Base at $97,735. After that, the drop-off is severe. Arbitrum manages $12,982. And then it gets grim.

Berachain, a chain that raised $142 million at a $1.5 billion valuation, generated $0 in fees over the past 24 hours. Sei, backed by $85 million from Jump Crypto and Multicoin Capital, also generated $0. Blast, which at its peak held $2.5 billion in TVL, generated $0. Movement, which raised $138 million, generated $0. And Somnia, which received $270 million in backing, managed $12. Not $12 million or $12 thousand. Twelve US dollars.

The total value locked figures paint a similarly bleak picture. Chains that collectively raised over $700 million in venture capital now hold less combined TVL than a single mid-tier DeFi protocol on Ethereum.

The Five Biggest Stinkers

To understand how the industry arrived at this point, it is worth examining five chains that exemplify the ghost chain phenomenon: projects that attracted significant funding, generated enormous hype, and have since failed to sustain meaningful usage.

1. Somnia: $270 Million Raised, $12 in Daily Fees

Somnia may be the single most egregious example of capital misallocation in the current cycle. The project, backed by Improbable and MSquared with investors including Andreessen Horowitz, SoftBank, and Digital Currency Group, received up to $270 million to build a blockchain optimised for metaverse and virtual world applications. The pitch centred on achieving one million transactions per second with sub-second finality, a technical claim that, even if achieved on a devnet, has proven entirely academic in the absence of actual users.

Somnia's mainnet launched in September 2025 alongside the SOMI token. Today, the chain holds $1.37 million in TVL, generates $12 in daily fees, and has a bridged TVL of under $1 million. The SOMI token trades at $0.16, giving the project a fully diluted valuation of $162 million, a figure that still looks generous for a chain with effectively zero economic activity. The DEX volume on the entire chain is $14,372 per day, less than what many individual traders transact in a single session on Uniswap.

The core problem with Somnia was always its thesis. The metaverse narrative that drove investment in 2022 and 2023 has not materialised as promised, and building a dedicated chain for virtual worlds assumed a demand that does not exist at scale. No amount of throughput matters if there is nothing for users to do.

2. Blast: From $2.5 Billion TVL to $0 in Daily Fees

Blast represents the purest case study in incentive-driven growth and its inevitable collapse. Created by Tieshun Roquerre (known as Pacman), the founder of NFT marketplace Blur, Blast launched in early 2024 with a simple but powerful hook: deposit ETH and stablecoins, earn native yield through Lido staking and MakerDAO's Treasury bill exposure, and qualify for a future airdrop.

The strategy worked spectacularly, for a while. Blast attracted $2.5 billion in TVL before its mainnet even launched, making it one of the fastest-growing L2s in history. At its peak in June 2024, the chain boasted 180,000 daily active users and a thriving ecosystem of DeFi protocols and applications. Paradigm led its $20 million funding round, and the industry watched closely.

Then the airdrop happened, and the exodus began. Users who had deposited solely for the token reward withdrew their capital en masse. Daily active users collapsed from 180,000 to under 4,000. TVL plummeted 98.6% from its peak to $34.9 million. Today, Blast generates $0 in 24-hour chain fees and negative revenue, meaning the chain is literally losing money to operate. Multiple projects built on Blast, including Blast Royale, shut down amid funding droughts.

3. Berachain: $142 Million Raised, Novel Consensus, Zero Fees

Berachain entered the market with genuine technical differentiation. Its Proof of Liquidity consensus mechanism, where validators stake liquidity pool tokens rather than native tokens to secure the network, was a novel approach to aligning network security with DeFi activity. The project raised $142 million in funding at a $1.5 billion valuation, with investors including Brevan Howard Digital, Framework Ventures, Polychain Capital, and Samsung Next.

The chain launched to significant fanfare and briefly achieved over $3.3 billion in TVL, driven by aggressive incentive programmes and a multi-token model involving BERA (the gas and staking token) and BGT (the governance token earned through providing liquidity). For a moment, it seemed like the flywheel was spinning.

It was not sustainable. Berachain's TVL has collapsed 97.2% from its peak to $91 million. The chain generates $0 in daily fees. The BERA token has fallen roughly 90% from its highs, which in turn reduced the value of the incentives meant to attract liquidity, creating a death spiral. On-chain data reveals that 83.7% of wallet addresses have made fewer than five transactions, indicating that the overwhelming majority of users were low-frequency participants: airdrop farmers, not genuine users. The foundation has undergone layoffs, and key developers have departed.

4. Sei: $85 Million Raised, an Identity Crisis in Progress

Sei launched as a Layer 1 blockchain explicitly optimised for trading, built on the Cosmos SDK and backed by $85 million from investors including Jump Crypto, Multicoin Capital, Coinbase Ventures, and Goldman Sachs alumni. The pitch was a chain purpose-built for orderbook-style exchanges, with a built-in matching engine and parallelised transaction processing.

The problem was that the market did not need a dedicated trading chain. By the time Sei launched, decentralised exchanges had largely converged on the automated market maker model rather than orderbooks, and the chains that did attract trading volume (Solana, Arbitrum, Base) did so because of existing liquidity and user bases rather than bespoke trading infrastructure. Sei's TVL peaked at $628 million but has since fallen 93.5% to $40.5 million. It generates $0 in daily chain fees.

In a telling sign of its predicament, Sei announced in 2026 that it would abandon its Cosmos-based architecture entirely and transition to an EVM-only chain by mid-2026. The pivot, branded as the Sei Giga upgrade, effectively concedes that the original thesis was wrong and that Sei needs to compete on EVM compatibility rather than specialised trading infrastructure. Whether this reinvention will attract users remains to be seen, but the track record of mid-cycle pivots in crypto is not encouraging.

5. Monad: $248 Million Raised, Still Too Early to Call

Monad occupies an unusual position in this analysis. The project raised $248 million at a $3 billion valuation, the largest funding round of any chain on this list, led by Paradigm with participation from Electric Capital, Greenoaks, and Coinbase. Unlike the other chains examined here, Monad only recently launched its mainnet, making it premature to declare it dead.

The numbers so far are mixed. Monad holds $362 million in TVL, which sounds respectable but represents a $3 billion-valued chain generating just $6,311 in daily fees. For context, that is roughly what a small-town car wash generates in revenue. The chain's TVL has remained relatively stable since launch (it has not experienced the dramatic post-airdrop collapses seen with Blast and Berachain) but it has also not shown the organic growth trajectory that characterised the early days of Solana or Base.

Monad's technical proposition, an EVM-compatible chain with parallel transaction execution and 10,000 TPS, is sound, but it faces the fundamental challenge of differentiation in an increasingly crowded market. With Base, Arbitrum, and the upcoming Ethereum Glamsterdam upgrade all targeting similar performance improvements within the EVM ecosystem, Monad must find a compelling reason for developers and users to choose it over incumbents with established network effects.

What Is Actually Working, and Why

The ghost chain graveyard stands in sharp contrast to the handful of blockchains that have achieved genuine, sustained economic activity. Understanding why these chains succeeded while hundreds of others failed is the most important question in the industry today.

Solana: $5.5 Billion TVL, $508,729 in Daily Fees

Solana has emerged as the primary alternative to Ethereum, generating more daily fees than any other chain except Tron. Its success stems from a combination of technical performance (sub-second finality and transaction costs measured in fractions of a cent) and a vibrant consumer application ecosystem. Solana hosts the majority of memecoin trading activity, the leading decentralised perpetual futures platforms, and a growing DePIN sector. Critically, Solana's usage is organic rather than incentive-driven. Users come for the applications, not for airdrop rewards.

Base: $4.1 Billion TVL, $97,735 in Daily Fees

Base is the clearest example of what actually works in the L2 space: distribution. As Coinbase's native Layer 2, Base has direct access to the exchange's 9.3 million monthly active trading users, a built-in funnel that no other L2 can replicate. This distribution advantage has translated into concrete results: $75.4 million in year-to-date revenue (accounting for 62% of all L2 revenue), $5.2 billion in stablecoin liquidity, and 1.3 million daily active wallets.

Aerodrome, the chain's dominant DEX, alone generated $160.5 million in revenue in 2025. Base did not need to bribe users with token incentives because it had something more valuable: a direct path from centralised exchange to on-chain activity. The lesson is clear. Distribution beats technology, every time.

Ethereum: $52.5 Billion TVL, $252,917 in Daily Fees

Ethereum's dominance is not accidental. Despite years of narrative about it being too slow and too expensive, Ethereum remains the settlement layer for the majority of high-value DeFi activity. Its $52.5 billion TVL dwarfs every competitor combined. The reasons are network effects, composability, and the deep liquidity pools that make it the default venue for institutional DeFi activity. The upcoming Glamsterdam upgrade, with its 200 million gas limit and parallel transaction processing, will likely reinforce Ethereum's position rather than undermine it.

Tron: $4.8 Billion TVL, $1.05 Million in Daily Fees

Tron generates more daily fees than any other blockchain, a fact that often surprises Western crypto observers. The reason is simple: Tron has become the dominant chain for USDT transfers, particularly in emerging markets across Asia, Africa, and Latin America. Tron processes more stablecoin volume than any other chain, and its low fees make it the preferred rail for remittances and cross-border payments. The lesson from Tron is that real-world utility, even a single dominant use case, is worth more than a thousand theoretical innovations.

What Separates the Living From the Dead

The pattern that emerges from this analysis is stark but instructive. The chains that have succeeded share a set of common characteristics that the ghost chains almost universally lack.

Distribution matters more than technology. Base's access to Coinbase's user base, Solana's vibrant developer community, and Tron's dominance in USDT transfers all represent genuine distribution channels. The ghost chains, by contrast, relied on token incentives and airdrop campaigns: artificial distribution that evaporated the moment rewards ended. Every chain that built its user base primarily through airdrops has seen catastrophic declines in activity once the incentives dried up.

Timing and network effects create winner-take-most dynamics. Ethereum, Solana, and Arbitrum all benefited from being early enough to establish deep liquidity pools and developer ecosystems. By the time chains like Sei, Berachain, and Somnia launched, the market was saturated. Developers had already chosen their platforms, liquidity was concentrated on established chains, and users had limited appetite for migrating to yet another ecosystem with unfamiliar wallets, bridges, and applications.

Real use cases beat theoretical performance. Tron does not win any beauty contests for blockchain architecture, but it processes more real economic value than chains with ten times the throughput. Similarly, Base's success is not because it is the fastest or cheapest L2. It is because users can go from buying crypto on Coinbase to using it on-chain in a single flow. The ghost chains optimised for benchmarks rather than user journeys.

Sustainability requires organic demand. Blast's trajectory, from $2.5 billion to $35 million, is the most dramatic example of what happens when growth is entirely incentive-driven, but the same pattern is visible across Berachain, Sei, and numerous smaller chains. A blockchain that cannot generate fees without subsidising usage has not built a product that people want. It has built a temporary promotion.

Where Does the Industry Go From Here

The ghost chain phenomenon represents one of the most significant misallocations of capital in crypto's history. Conservatively, more than $5 billion in venture funding has gone into blockchain infrastructure projects that now generate negligible economic activity. The opportunity cost, measured in developer talent, investor attention, and industry credibility, is incalculable.

For venture investors, the lesson is that infrastructure plays in crypto are subject to extreme power law dynamics. The market does not need 200 Layer 1 and Layer 2 chains any more than the internet needed 200 operating systems. The returns will continue to concentrate in the handful of chains that have achieved genuine network effects, and the long tail of funded-but-unused chains will quietly wind down over the coming years.

For developers and founders, the message is to build where the users already are rather than trying to bootstrap an entirely new ecosystem from scratch. The era of launching a chain and hoping that developers and users will follow has conclusively ended. The projects that will succeed going forward are those building applications on chains that have already solved the distribution problem.

And for the ghost chains themselves, the path forward is narrow. Some, like Sei, are attempting radical pivots. Others will gradually fade as treasury funds deplete and team members move on. A few, perhaps Monad among them, may yet find traction if they can identify a genuine wedge that differentiates them from the established players. But the data is clear: in the blockchain industry, as in most technology markets, the winners are few and the graveyard is vast.

All data referenced in this article was sourced from DeFi Llama (defillama.com) on 7 April 2026. Funding figures are drawn from public announcements and CryptoRank.io.